What is a Cryptocurrency Mining Farm?

crypto mining

Bitcoin was mined with the CPUs of enthusiasts’ computers in the early days, before exchanges, mining pools, and worldwide adoption. The first Bitcoin miners had a decent chance to win their block reward operating solo, but these days you’d be hard-pressed to do so with anything short of a mining farm.

Most of the original cryptocurrencies could be mined. It’s on the wane now, but there are still mineable cryptos that use a consensus mechanism called “proof of work.” Proof of work depends on a certain level of difficulty, which in turn requires a certain amount of computing power to mine.

So, what is cryptocurrency mining, and why are there entire farms devoted to the task? Let’s find out.

What is Cryptocurrency Mining?

Another name for a blockchain is a distributed public ledger. This describes a blockchain as being a record of transactions that exists on a decentralized public network of computers called nodes.

Transactions made on this network are grouped into what’s called a “block.” It also contains a cryptographic hash of the previous block’s contents. This gives the blockchain its famous quality of immutability—changing a single transaction in the past would change the block’s hash and break the established chain.

This hashing and grouping of transactions together into blocks is called “block production.” Blocks are also verified once they are produced. In a proof-of-work cryptocurrency, block production and verification are done by nodes called miners.

These miners race with each other to solve the hash, and miners with more processing power (or hashing power) are at a distinct advantage since they can try more solutions faster. Still, it’s not impossible for a solo miner with low hashing power to win a block, even on a high-difficulty network like Bitcoin.

All blockchains incentivize miners to get on board and start producing blocks. This is done via a chunk of network currency called the block reward. The miner who wins the race to produce a block on Bitcoin, for instance, wins a block reward of 6.25 BTC currently.

What are the Chances of Winning the Block Reward?

If you’re running a single computer or just a few machines in your mining farm, you can compare cryptocurrency mining to a lottery. Your total hashing power serves as the ticket guaranteeing entry to the lottery.

Mining is even better since every single block is a lottery, and you can keep your computer going for days if you want. In crypto mining, the odds aren’t as bad as with a lottery, and there are no intermediaries who take their cut before paying out.

The problem is that there are a lot of miners vying for that vaunted BTC block reward. Even if you look at proof of work cryptocurrencies with far smaller market capitalization, the block reward can be worth a pretty penny.

Where there’s value to be gained, there’s competition. And with Bitcoin’s block reward, there is a lot of competition—to the point where only 270 of the 700,000+ blocks in history have been won by solo miners operating rigs or small farms of their own.

Why is Proof of Work Important?

To underline proof of work’s importance, we need to go back to the definition of a blockchain, i.e., a distributed public ledger. As mentioned previously, one miner produces the block, and the rest of the miners validate it.

This can be viewed as the whole, or majority, of the distributed network coming to agreement on the truth of what happened. Proof of work mining is the mechanism by which they do this.

There are other consensus mechanisms, such as proof of stake, proof of authority, proof of history, and even proof of burn, but proof of work was the first to rise to prominence. It is used in Bitcoin and countless other cryptocurrencies and is considered “battle tested.”

Proof of work mining is often criticized for its energy intensity, but proponents also point out that significant work is being done to generate coins. They can’t be created out of thin air, requiring much power and energy to mine them.

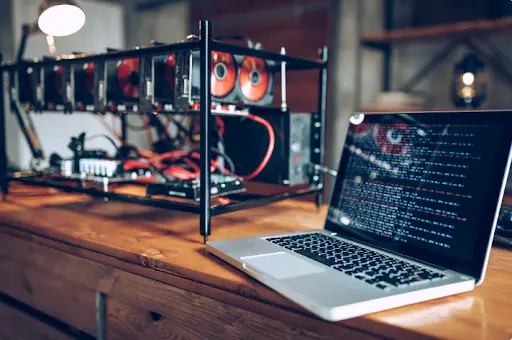

What is a Mining Farm?

A mining farm is the term given to the space used by a crypto miner to house their mining operation. As you can imagine, this could be anything from a closet or small room with one or a few PCs, GPUs, or ASICs to an entire warehouse or complex with hundreds of thousands of dollars worth of computers.

Just as your PC needs decent cooling when you use it for mining, gaming, or productivity, cooling is a big part of a mining farm. This is true for small-scale mining farms since even a rig made up of a few GPUs can run very hot without good cooling.

So, a mining farm generally refers to a space, however large, used to house and cool machines devoted to the task of mining proof-of-work blockchains.

There are some famous mining farms out there, such as Genesis Mining, based in Iceland, and Washington’s GigaWatt. They can also come in some very unusual forms and locations, and this was even the subject of a feature in Architectural Digest.

How to Set Up a Mining Farm?

Just as with any business, there are several things to consider when setting up a mining farm. The main considerations are starting capital requirements, fixed costs, and the longevity of your business model.

When deciding how much starting capital you’ll need, you’re mostly looking at the cost of purchasing the computer hardware you need for mining. This may be one or more ASICs or multiple GPUs, along with the cooling gear and other peripherals to go with your rig.

Despite the fact that starting capital requirements could be quite hefty, it's the fixed costs that could make or break your mining farm. Electricity is the one main ingredient all mining farms use, but it’s not the same price everywhere.

Areas with cheaper electricity are therefore advantageous for mining, and there’s a reason that many mining farms also have their own renewable energy sources, such as solar power arrays.

Once you’ve factored in rent and maintenance costs on top of electricity, you’re all set. Now you need to figure out how much you'll make and if it makes sense to go ahead with the plan.

This is where longevity comes in, as well. If you think proof of work mining won’t last for very long, it’d be silly to spend lots of money on an array of ASICs that’d then become worthless. GPUs have resale value, but gamers are fully aware of how crypto miners use their cards and won’t pay top dollar for cards used in mining farms.

So, once you’ve got your hardware and mining software set up and your ROI worked out, what remains is to decide if you want to forge ahead solo or join a mining pool.

What is a Mining Pool?

Mining pools give miners a greater chance of earning rewards by combining the hash power of all participants, allowing the hash function to be processed much faster. This helps small-scale mining farms earn a regular, reliable income rather than hoping to win the block reward by themselves.

There are several payout models for mining pools, the first of which is called the “proportional” mining pool. Participants receive “shares” of the pool in these pools based on how much of the pool’s total hash power they have contributed. When the pool finds a block, it pays out block rewards to miners depending on how many shares they hold.

Another common scheme is the “pay-per-share” pool. These pools also give miners shares, but they also provide instant payouts, irrespective of when the block is found. This is a versatile and quite compelling pool model for miners because shares can also be exchanged for payouts at any time.

The third major type of mining pool is called the “peer-to-peer” mining pool. These aim to combat the issue of centralization in mining pools by integrating a separate pool-specific blockchain. The objective of these pools is to prevent the pool operators themselves from misbehaving. It also removes any single point of failure from the pool itself.

Advantages of Joining a Mining Pool

If you have a mining farm, you’re probably generating a decent amount of hash power alone. Still, there are reasons why you may want to consider joining a mining pool:

- Guaranteed payout. It’s difficult to make it as a solo miner, and the odds of winning a block reward on a blockchain like Bitcoin are remote if you only have a small mining farm. In fact, there’s no guarantee of ever winning a block reward, so it’s anything but a stable source of income. A mining pool, especially one with a decent amount of the blockchain’s total hash power, can guarantee an income.

- Regular payouts. Mining pools make it so that you can’t win and claim a block reward outright, but they directly convert mining time into cryptocurrency. You can earn a regular income from mining, especially if you use a pool with a good payout scheme.

Disadvantages of Joining a Mining Pool

That said, mining pools have come under plenty of criticism over the years. Let’s take a quick look at what’s been said:

- Centralization. Cryptocurrencies are meant to be decentralized, but mining pools centralize hash power by their very nature. Given the way mining works, it’s the only way for small-scale mining farms to earn an income, although innovations like peer-to-peer mining pools help combat this sort of criticism.

- Single point of failure. Attacking or compromising a big mining pool at its head could adversely affect the network, and mining pool operators could also try and cheat. If a handful of the top pools, or even the two biggest pools, decide to collude, Bitcoin could be compromised.

How to Join a Mining Pool with Your Mining Farm

So, if you’ve decided that you like the prospect of earning a regular income from mining via a mining pool, here’s a brief guide on how to get started.

#1. Pick a Cryptocurrency

If there’s a particular proof of work cryptocurrency you have faith in and want to accumulate, mining is a great way to do it. On the other hand, you could also decide that certain coins are particularly liquid and will hold their value better than others, making them a good choice to mine.

Still, there are several cryptocurrencies, such as Ergo and Ravencoin, that you can mine with a GPU-based farm. Monero is also a great option and can be mined in parallel with the others if you’re stringing entire PCs together since it requires a CPU instead.

#2. Buy Mining Equipment

Cryptocurrencies like Bitcoin require additional hardware since they aren’t ASIC-resistant. ASICs are specialized mining computers that push out a lot of hashes, eclipsing even the very best of GPUs, but they can sometimes be tricky to acquire.

#3. Review Available Mining Pools

Check out the mining pool stats on offer, what sort of hash power they have, and how they work. Ensure that the pool is transparent and that the payout schemes are in order.

If you’re connecting with a comparatively low-end mining farm or just your home PC, check the minimum payment threshold—you should be able to find a pool that’ll pay you every few days at the very least, even if you’re not mining 24/7.

#4. Choose and Join a Mining Pool

Once you’ve found a mining pool that suits you, join up. Some pools require registration since they operate as a service, but with most pools, it’s just a matter of downloading their mining pool software.

If you don’t have a crypto wallet at this point, remember to get one! You’ll have to configure the mining pool software with your wallet address to receive any payouts.

Key Takeaways

The term “mining farm” refers to an area used for the express purpose of cryptocurrency mining. It’s set up in such a way as to house, cool, and power any number of ASICs or GPU rigs.

Crypto mining and miners, in general, are the backbone of proof-of-work blockchains such as Bitcoin because it is their work and computational power that secures these networks. If a network isn’t supported by enough miners, it could be attacked and compromised very easily.

This level of importance means that miners are very well compensated, however. This is done via a block reward, which all the miners compete for. It’s not very likely for small mining farms to win this block reward, so they’re often the best candidates to join a mining pool for regular rather than variable income.

Mining Farm FAQs

What is a mining farm?

A mining farm is an area, be it an entire building or simply a room in your house, dedicated to crypto mining. It houses your mining equipment, meaning computers and cooling.

What is proof of work?

Proof of work is a consensus mechanism for blockchains that requires mining. Proof of stake networks can be validated by a single server, so there’s no need for an entire farm, but proof of work needs plenty of hash power.

Is a mining farm the same as yield farming?

No. Yield farming is prevalent in Decentralized Finance (DeFi) and has nothing to do with hardware-based proof of work mining.

Can you join a mining pool with your mining farm?

You absolutely can. Mining pools have their faults, but they’re a great way to improve your odds of at least sharing the block rewards of a network consistently, rather than going days, weeks, months, or even years without a payout.